Labor rejects 6pc rise in health insurance premiums

Health Minister Mark Butler has rejected the health insurance industry’s request to deliver the biggest premium rise in at least six years, as the government tries to quell voter discontent over the rapid increase in the cost of living.

As part of the annual negotiations for premium increases, which the minister must approve for each provider, the country’s 31 insurers requested annual rises that could have delivered an average premium hike as high as 6 per cent.

But Mr Butler told The Australian Financial Review he was not inclined to approve providers’ proposed premium increases based on the information currently provided.

“I’ve written to every private health insurer, directing them to have another go and put forward a more reasonable figure that considers their years of record profits and the declining proportion of premiums they return to customers, particularly while household budgets are under pressure,” he said.

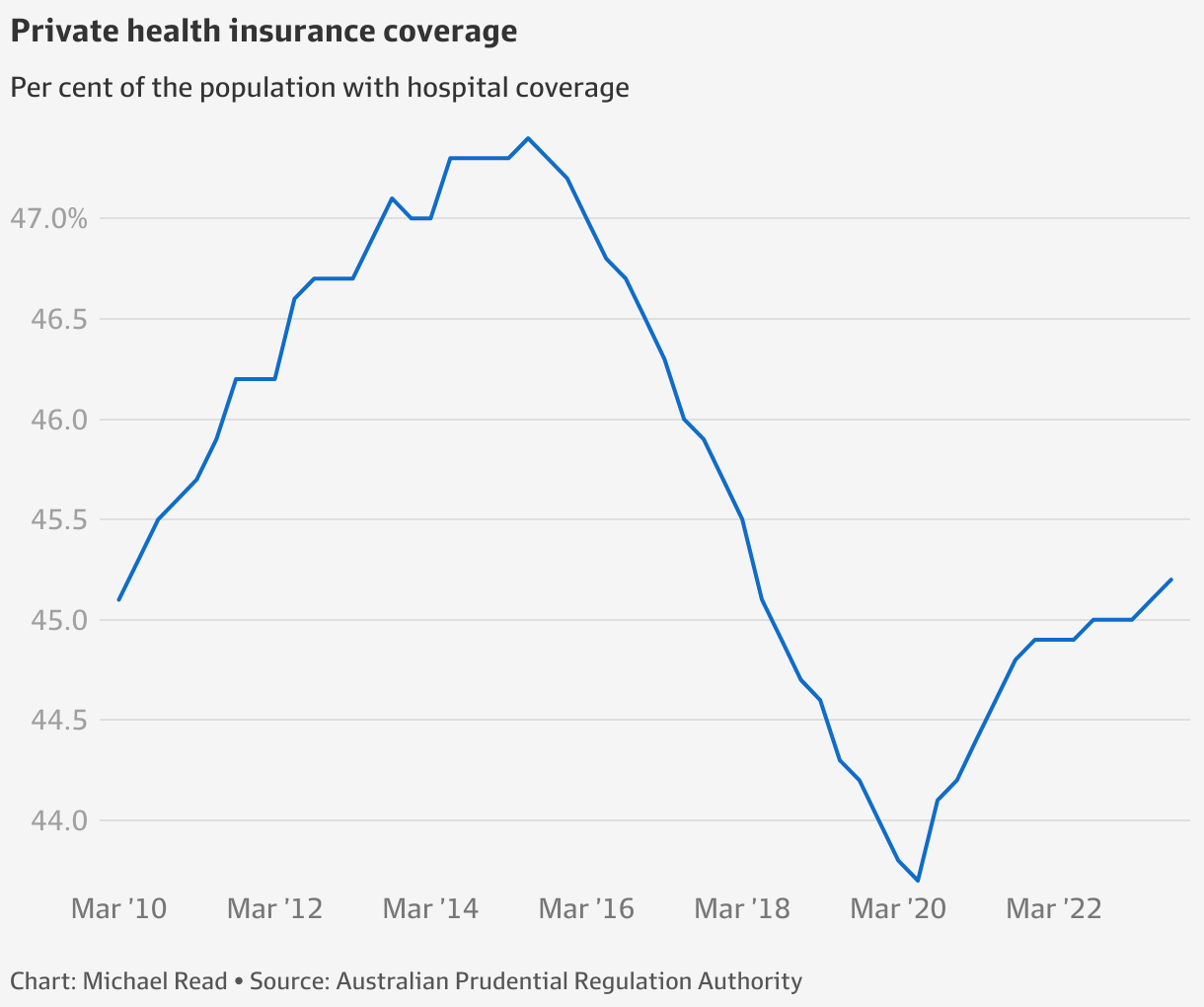

The health insurance industry was pushing Mr Butler to wave through the biggest premium increase since at least 2018, which would have hit the 14.6 million Australians – or 55 per cent of the population – who have hospital or extras cover.

NIB chief executive Mark Fitzgibbon said he thought the industry-wide average premium increase request for 2024 was between 4 and 6 per cent, given how fast claim costs were rising.

“We ultimately price to reflect our underlying claims experience. So, with things quickly returning to normal … we expect claims inflation will resume its past trajectory, which is somewhere between 4 per cent and 6 per cent,” he told The Australian Financial Review.

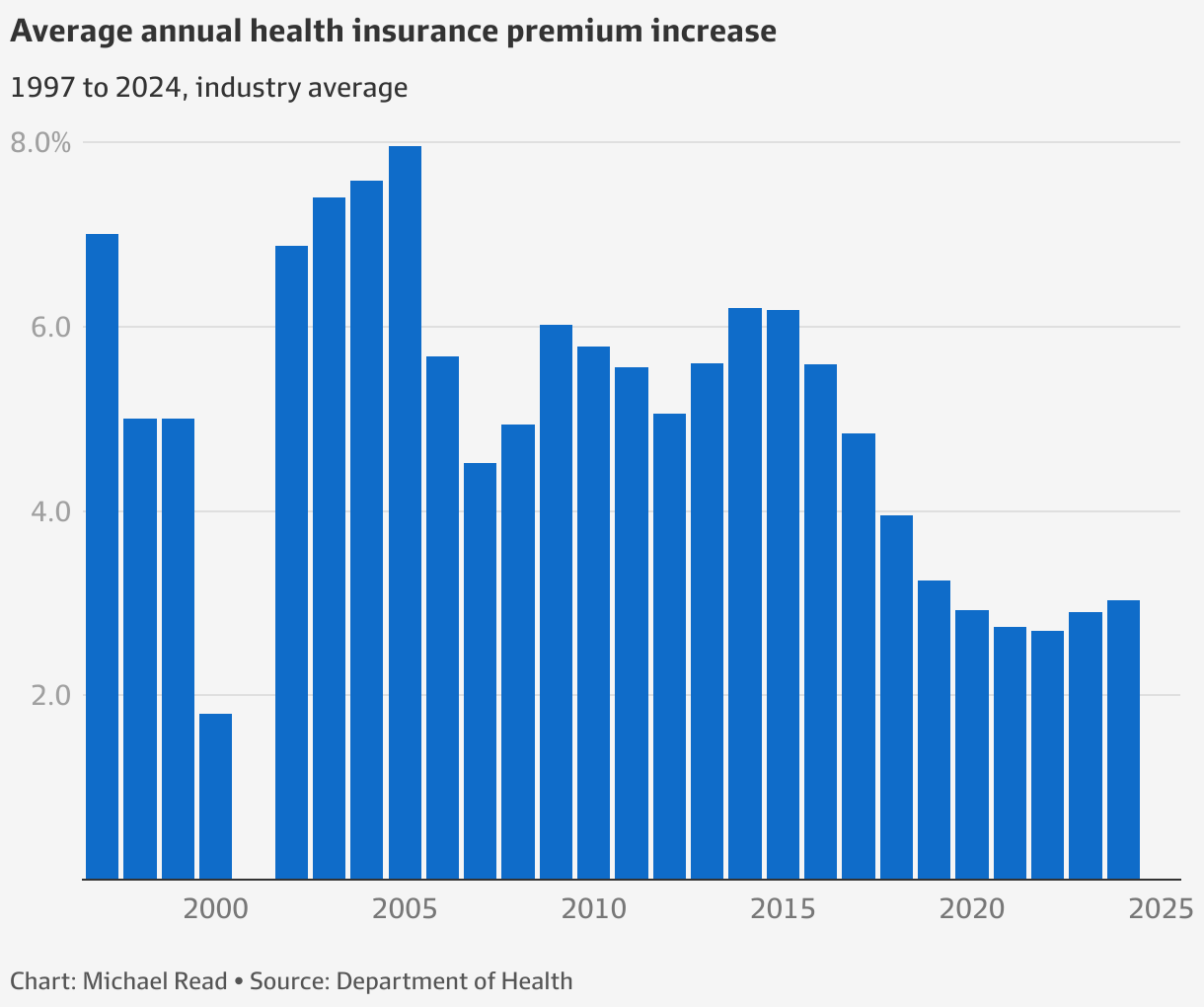

Health insurance premiums increased by a comparatively modest 2.9 per cent in 2023, and by 2.7 per cent in both 2021 and 2022.

An average premium rise as high as 6 per cent was a non-starter for the Albanese government, as it grapples with widespread community concern around the cost of living.

The latest The Australian Financial Review/Freshwater Strategy poll, released on Monday, found cost of living was the single largest concern among voters, with 71 per cent of respondents wanting the federal government to focus on the issue. That was streets ahead of housing and accommodation, which was the second-highest concern for voters at 43 per cent.

The government has lost five points since September as the preferred manager of cost of living and now trails the Coalition by 28 per cent to 33 per cent on the issue. One year ago, Labor had a 13-point led over the Coalition on the cost of living.

Prime Minister Anthony Albanese said on Monday the government was getting advice from Treasury about how it could deliver further relief to households at the next budget in May 2024.

“We understand that so many people are doing it tough. Inflation affects the poor more than anyone else,” he told ABC radio.

“It inversely affects people who can least afford to pay. And that is something we’re very conscious of. That’s why fighting inflation has been our main priority.”

Premiums need to be ‘justified’

Mr Butler said during a global cost of living crunch, it was his responsibility to ensure that premium increases were “justified and proportionate”.

Approved premium increases will come into effect on April 1, 2024.

The government believes the health insurance industry can afford to deliver a smaller increase in premiums than it has proposed.

The sector’s net profit more than doubled last financial year to $2.19 billion from $1.04 billion, according to the Australian Competition and Consumer Commission.

The Australian Medical Association’s 2023 private health insurance report card found that gross margins for hospital insurance represented about 18 per cent of premiums paid in 2022-23, representing a $1.36 billion increase in gross margins on 2020-21.

But with total health insurance payouts increasing 10.4 per cent over the 12 months to September, Private Healthcare Australia chief executive Rachel David said it will be impossible to maintain the extremely low premium increases of recent years.

“Like many parts of the economy, private hospitals have been hit by inflation and are grappling with the spiralling costs of recruitment, power and food,” Dr David said.

Despite COVID-19 driving some efficiencies in the healthcare sector, NIB’s Mr Fitzgibbon said healthcare spending was like “whack a mole”.

“Where we achieve efficiencies in one area, we seem to find somewhere else to spend them,” he said.

“The combination of an ageing society, the rise of chronic diseases like diabetes and obesity, and then the tendency for consumers to spend more and more of their income on health care means that we are still going to see growth,” he said.

Riding the pandemic wave

Dr David pointed to the 13.1 per cent surge in medical device use over the past four years as particularly concerning, given broader medical services only increased 1.3 per cent over that time.

“Overpriced and overused medical devices are affecting premiums,” she said.

“Over the next year, we will be working hard with government to crack down on medical device costs and dubious medical procedures that do more harm than good, so we can maximise value and affordability for the 14.7 million Australians contributing to their healthcare via private health insurance.”

The pandemic was a boon to insurers’ bottom-lines, with fewer consumers making claims due to a pause on elective surgery, leading the sector to build up large cash reserves.

The sector returned $4.3 billion to customers during the pandemic in the form of cashbacks and deferred premium rises, due to the savings from the low level of claims made during lockdown.

But hospital and extras claims have risen sharply since the end of the pandemic, according to data from the Australian Prudential Regulation Authority (APRA).

Episodes of hospital care funded by insurers jumped 9.6 per cent in the 12 months to September, while extras claims on services like dental and optical lifted 5.4 per cent.

Mr Fitzgibbon conceded there was a risk that a large rise in premiums next year would force some Australians to dump their private health insurance cover, potentially signalling the end to the resurgence in private health coverage.

About 840,000 Australians have signed up for private health insurance since September 2020, according to data from the Australian Prudential Regulation Authority (APRA).

Mr Fitzgibbon said there were several factors driving the increase in health insurance coverage.

“One is population growth. Immigrants tend to have a high propensity to take out health insurance,” he said.

“There’s an increased consciousness in the community about the risk of disease and the need for protection because of COVID-19.

“There’s obviously a public hospital waiting list effect. People are concerned about long waiting periods in the public hospital system.“

Introducing your Newsfeed

Follow the topics, people and companies that matter to you.

Find out moreRead More

Latest In Economy

Fetching latest articles