Compare the pair: Retail super closes the fee gap

The performance gap between industry and retail superannuation funds is narrowing, raising the prospect of a fightback by for-profit super after the savaging wrought by the banking royal commission.

Some retail offerings are achieving better investment results for lower fees than industry funds in the no-frills $996 billion MySuper segment, which is where most Australians have their money, Rainmaker research director Alex Dunnin said.

Some retail offerings are achieving better investment results for lower fees than industry funds in the no-frills MySuper segment. Getty

“The whole ecosystem now punishes poor performance and expensive products,” he said. “Right now, the average retail MySuper product is outperforming the average not-for-profit MySuper product, so the tribal wars are done.”

In the year to October 31, the retail MySuper index compiled by Rainmaker outperformed the not-for-profit MySuper index, returning 4.7 per cent versus 4.5 per cent. The small outperformance by retail funds was mainly due to their higher allocation to shares, which have rallied in the latter part of the year.

But the modern retail fund was a recent phenomenon and for-profit funds would have to prove they could maintain their competitiveness over decades rather than a single year and in favourable market conditions, Mr Dunnin said.

The top 10 performing balanced MySuper options for the 10 years to June 30, for example, were all industry funds, with Hostplus topping the ladder despite having comparatively high fees.

Over time, industry funds consistently outperformed retail funds because their heavy unlisted asset exposures cushion their equities portfolios from bad years.

In good news for Australia’s 15.6 million super savers, performance testing and the ban on financial advice commissions helped bring average fees down in the industry and retail segments to just 0.93 per cent, or the equivalent of $32 billion in 2022-23.

Fees could drop further still with further adoption of low-cost index investing and competition from new entrants such as Vanguard, which runs one of Australia’s cheapest super funds and has indicated further cuts in the new year.

Vanguard was the first index investor to move into the superannuation market last year, but local exchange-traded fund outfit BetaShares has since followed.

Vanguard’s fee is 0.58 per cent, but managing director Daniel Shrimski hinted even that was too high. “We’re already looking at what we will do over the next few months on fees, and we already think there’s an opportunity for us to modify what our current fees are [as we grow],” he told The Australian Financial Review.

Rise of indices

The presence of index funds was being felt elsewhere, too.

“If you look at the returns coming out of Colonial First State’s MySuper, they are market-leading and the engine underneath is BlackRock,” Mr Dunnin said.

After the royal commission, private equity firm KKR purchased a majority stake in Colonial First State and injected $430 million to help upgrade systems and rebuild the company’s reputation.

Last year, the prudential regulator found Colonial First State to be among the operators managing “significantly poor” default super products and the company responded by engaging BlackRock to help manage its investments.

Vanguard managing director Daniel Shrimski has hinted at further fee reductions. Luis Enrique Ascui

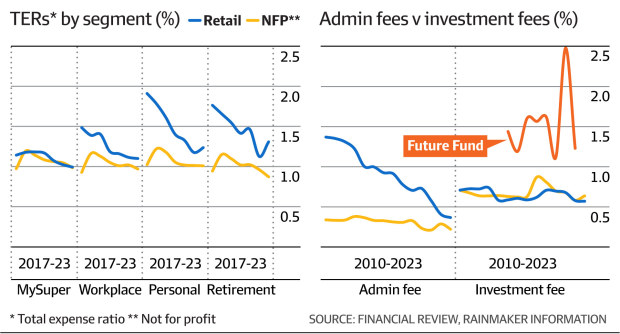

Average fees across retail MySuper products were 1.01 per cent compared to 1 per cent for industry funds in the 2022-23 financial year.

“Consumers are benefiting from domestic superannuation funds lowering their fees to become more competitive,” said Blake Briggs, the chief executive of the Financial Services Council, which represents retail funds.

“Global wealth businesses are also competing to establish their presence in the market and bring global investment expertise.”

Rainmaker has not examined the choice market, where there are many thousands of bespoke investment mixes on offer, mostly by retail funds.

Mr Dunnin said a major strategic threat for retail super funds, especially those hosted on platforms, was their poor results on the Your Future, Your Super performance test for “trustee-directed products”, where one-quarter of platform products assessed by the Australian Prudential Regulation Authority failed.

“Platform operators are yet to face up to the implications of these test results given the dire impacts the MySuper performance test had on that sector,” he said.

The government said this month it was looking at reforming the performance test, with industry funds leveraging their $1 trillion-plus asset pool to push for an overhaul, despite the fact it had driven down fees.

Funds said the test, which has been criticised for encouraging short-term investing and benchmark-hugging, discouraged them from investing in “nation building” areas such as affordable housing and the energy transition. Any overhaul would likely focus on the returns portion of the test rather than lessening the scrutiny on fees.

Higher expectations

Super funds faced a challenge to keep fees down given the government is demanding improvements to customer service and retirement advice. Mr Dunnin said.

“For fees to get lower, funds might squeeze their admin fees,” he said. “But given all the pressures on them to build more robust systems, handle the coming sustainability reporting onslaught – which is going to be immensely challenging even for the mega funds – innovate, provide advice and create new retirement solutions, this is a tough ask.”

The “easier route” might be reducing investment fees, as the growth of indexing, the rise of internal management – and the resulting pressure on investment managers – drove down these costs anyway.

Among non-MySuper options, retail funds on average still charge far more than industry funds. Their personal and retirement fees were much higher, while their workplace fund fees were slightly higher.

Profit-to-member funds hold 54 per cent of funds under management in the super sector but only account for 55 per cent of fee revenue, according to Rainmaker, while retail funds hold 21 per cent of savings but pull in 27 per cent of fees.

There is $1.1 trillion in 13 million industry super accounts, according to the Association of Superannuation Funds of Australia, compared to $690 billion in 6.5 million accounts in retail funds.

“Not-for-profit funds weren’t successful because they were smarter – they were on the right side of history,” Mr Dunnin said.

“Their funds are directly distributed to consumers through employers, meaning they never needed to charge the high fees required to pay for adviser commissions.

“The money is also stickier, so they could invest in high-return, long-term assets classes. This enabled them to evolve into really well-oiled machines. When the retail folks do the same thing, they get similarly good results.”

Introducing your Newsfeed

Follow the topics, people and companies that matter to you.

Find out moreRead More

Latest In Superannuation & SMSFs

Fetching latest articles